Asset Monetisation in India: A Complete Guide to How It Works and Why It Matters

As India navigates a complex fiscal landscape — marked by ambitious infrastructure spending targets, post-pandemic revenue pressures, and the persistent challenge of bridging the disinvestment gap — asset monetisation India explained has become one of the most consequential topics in public finance. Unlike outright privatisation, asset monetisation offers the government a structured pathway to unlock value from existing public infrastructure without permanently transferring ownership. With the National Monetisation Pipeline (NMP) still the cornerstone of India's medium-term fundraising strategy, and with fresh momentum building to compensate for slower-than-targeted disinvestment receipts, understanding the mechanics, implications, and limitations of this approach is essential for every banking and finance professional in the country.

What Is Asset Monetisation and How Does It Differ from Privatisation?

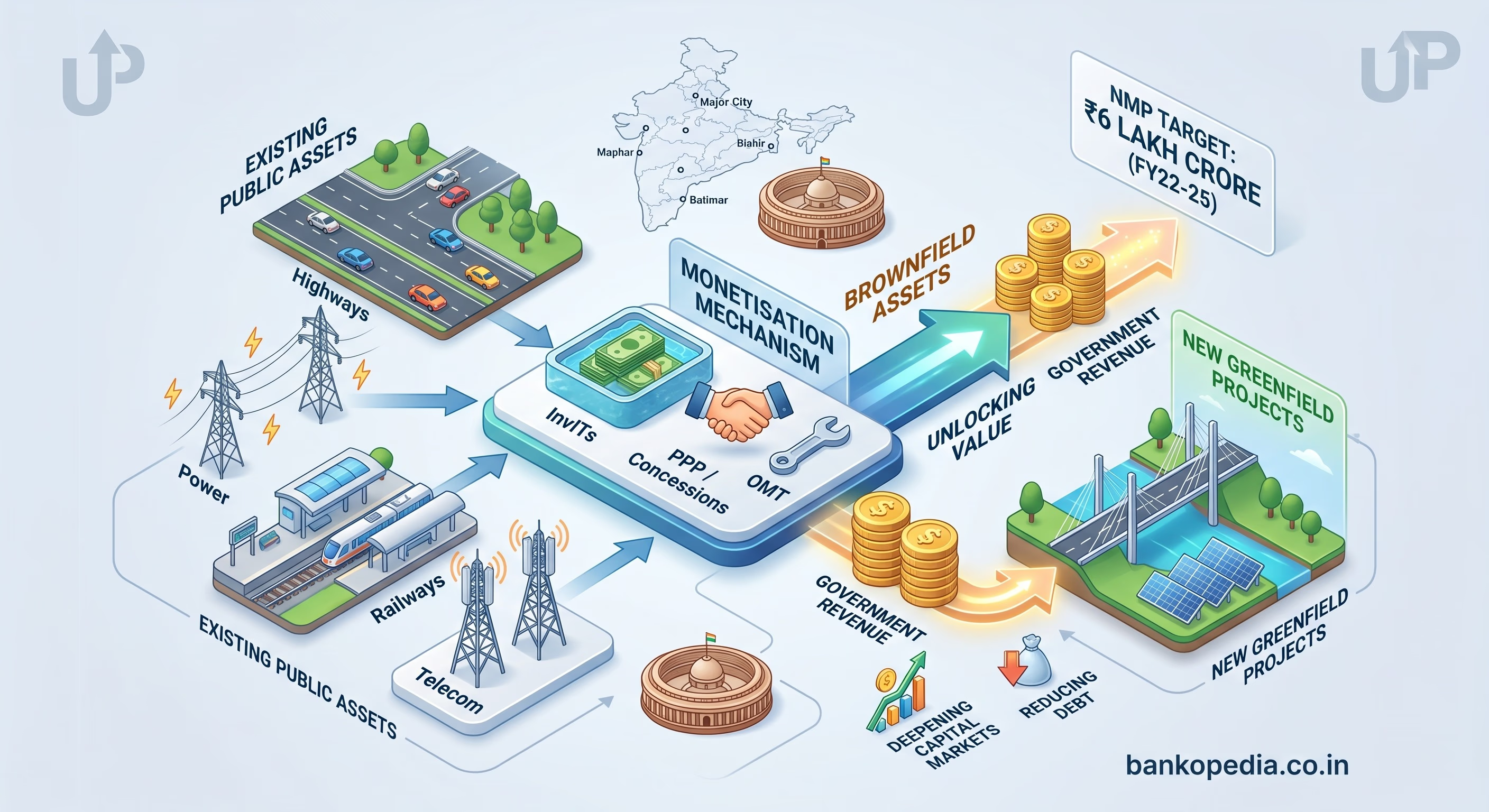

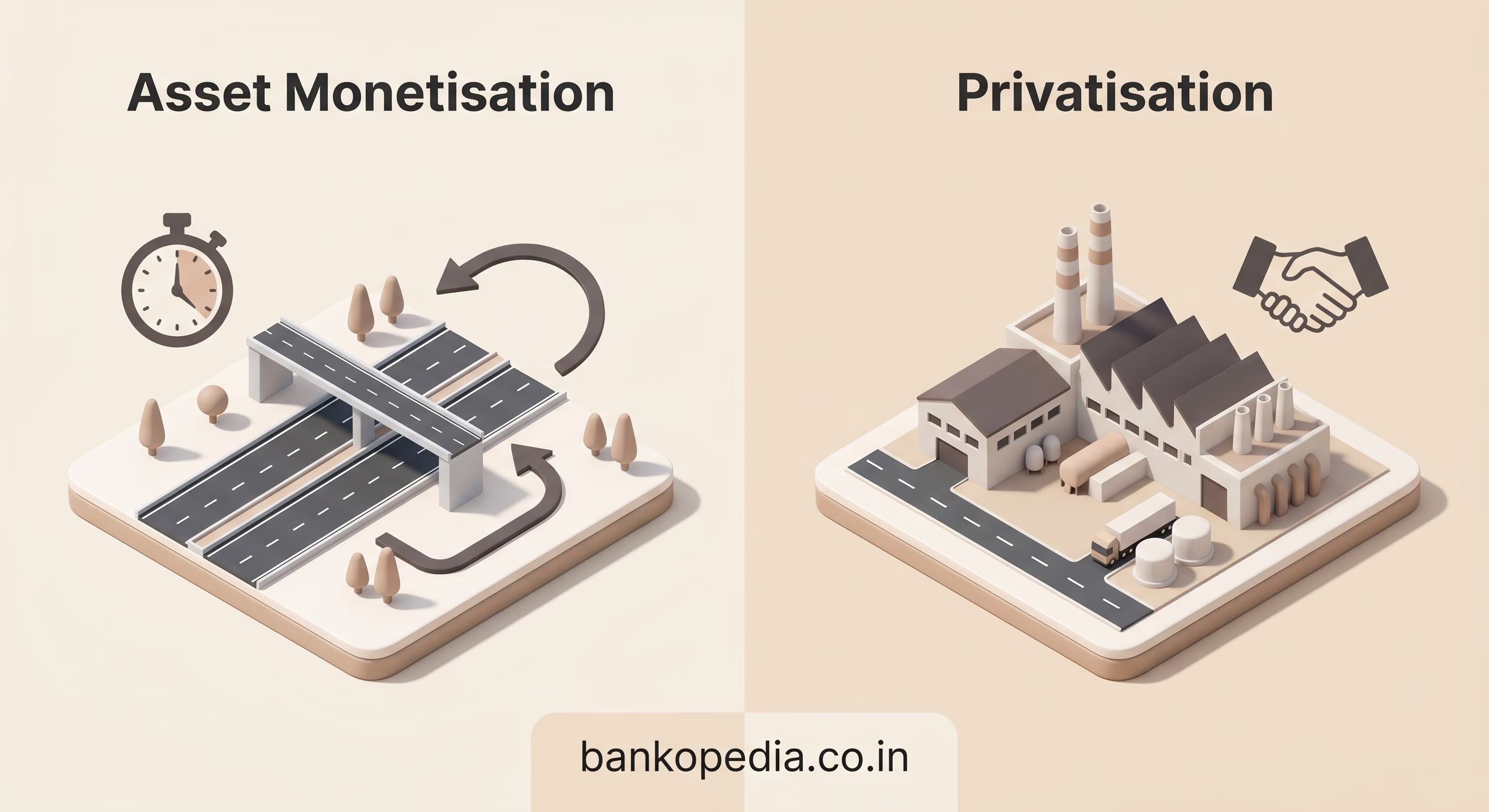

At its core, asset monetisation is the process by which the government or a public sector entity transfers the right to use, operate, and derive revenue from an existing asset to a private party for a defined period — while retaining the underlying ownership of the asset. Think of it as a long-term lease rather than a sale. The private operator pays an upfront fee or periodic concession charges, runs the asset efficiently to recover its investment, and hands it back to the government at the end of the contract tenure.

This is fundamentally different from privatisation, where ownership itself is transferred, often permanently. In privatisation, the government sells its equity stake — partially or fully — in a public sector undertaking (PSU), effectively ceding long-term control. The proceeds are a one-time inflow, and the strategic direction of that enterprise shifts to private hands indefinitely.

Asset monetisation, by contrast, is a time-bound, rights-based transaction. The government retains the title, the asset reverts after the concession period, and the public exchequer can potentially monetise the same asset again in a future cycle. This makes it particularly attractive for brownfield infrastructure — assets that are already built, operational, and generating steady cash flows, such as highways, transmission lines, gas pipelines, airports, and railway stations.

"Monetisation of assets is not about selling the family silver. It is about sweating existing assets more efficiently while freeing up capital for new greenfield investments." — A framing often used by NITI Aayog in its policy communications on the NMP.

The most common structures used in asset monetisation in India include:

Toll-Operate-Transfer (TOT): Used extensively by NHAI for highway bundles, where a private entity pays a lump sum upfront for toll collection rights over a specific road stretch.

Infrastructure Investment Trusts (InvITs): Public or private trusts that pool infrastructure assets, issue units to investors, and distribute the cash flows. SEBI regulates InvITs, and this structure has been used by PowerGrid, NHAI, and Gas Authority of India Limited (GAIL).

Real Estate Investment Trusts (REITs): Similar pooled structures for commercial real estate, regulated by SEBI.

Operate-Maintain-Transfer (OMT): The private operator manages an asset for a fee or revenue share without an upfront capital payment.

Public-Private Partnerships (PPP) under concession agreements: Broader framework covering airports, ports, and urban infrastructure.

It is also important to distinguish asset monetisation from stressed asset resolution, which operates in an entirely different domain. When Sammaan Capital recently sold a ₹5,000 crore loan portfolio to Arcil (Asset Reconstruction Company (India) Limited), a leading stressed loan aggregator, that was a balance sheet clean-up exercise under the securitisation and asset reconstruction framework — not infrastructure monetisation in the government sense. However, the underlying principle of unlocking trapped value from non-performing or underutilised assets shares a common philosophical thread.

National Monetisation Pipeline: Key Sectors and Targets

Launched in August 2021 by NITI Aayog in collaboration with the Ministry of Finance, the National Monetisation Pipeline (NMP) set an aggregate target of ₹6 lakh crore worth of core asset monetisation over four fiscal years — from FY2022 to FY2025. The pipeline spans 13 infrastructure sectors and covers assets held by more than 20 Central Government ministries and CPSEs (Central Public Sector Enterprises).

Sector-Wise Breakdown of the NMP

The NMP is not evenly distributed. A handful of sectors account for the lion's share of the identified pipeline:

Roads (NHAI and MoRTH): Approximately ₹1.6 lakh crore, making it the single largest component. NHAI's TOT programme and InvIT structure are the primary vehicles.

Railways (Indian Railways and RLDA): Around ₹1.52 lakh crore, covering railway stations, freight terminals, hill railways, and stadiums. The Indian Railway Finance Corporation (IRFC) plays a supporting role in financing.

Power (transmission and generation): Roughly ₹85,000 crore, led by PowerGrid Corporation's InvIT, which was one of the earliest large-scale successes of the NMP framework.

Natural gas pipelines (GAIL, IOCL): About ₹24,462 crore, leveraging InvIT structures for long-distance trunk pipelines.

Telecom (BSNL and DoT towers): Approximately ₹35,100 crore, including passive infrastructure and optic fibre networks.

Airports (AAI): Around ₹20,782 crore, building on the already successful privatisation of major airports like Mumbai and Delhi.

Ports, mining, urban real estate, warehousing, and sports stadiums constitute the remainder of the pipeline.

Progress and the Disinvestment Gap

Actual execution of the NMP has been uneven. While some sectors — particularly roads and power transmission — have recorded tangible progress through InvIT issuances and TOT bundles, Railways monetisation has faced significant operational and stakeholder complexities. The government has increasingly looked at asset monetisation to bridge the gap created by consistently missing its annual disinvestment targets. In several recent budgets, the government has fallen well short of its headline disinvestment numbers — a shortfall that asset monetisation receipts are expected to partially offset.

This recalibration of strategy reflects a pragmatic reality: outright sale of PSU equity requires market timing, investor appetite, and political will — all of which can be in short supply simultaneously. Asset monetisation, by design, is more structurally predictable, especially when underpinned by robust concession frameworks and regulated instruments like InvITs.

How Asset Monetisation Affects Government Borrowing and Capital Markets

The fiscal arithmetic of asset monetisation is straightforward in principle: if the government can raise ₹1 lakh crore through monetisation receipts in a given year, it reduces its gross market borrowing requirement by a corresponding amount — or alternatively, creates headroom for higher productive spending without breaching the fiscal deficit target.

Impact on Government Securities and Bond Markets

India's government securities (G-Sec) market is dominated by institutional players — commercial banks (which hold G-Secs for Statutory Liquidity Ratio compliance), insurance companies regulated by IRDAI, provident funds, and increasingly foreign portfolio investors (FPIs). When the government borrows less from the market because monetisation proceeds supplement revenue, the supply of G-Secs is moderated. This can have a softening effect on bond yields, reducing the crowding-out of private sector borrowing.

The RBI, as the government's debt manager, closely monitors the quantum and timing of market borrowings through the calendar it announces each April. Any material shortfall in non-debt capital receipts — including monetisation — can force the RBI and the Finance Ministry to revise borrowing calendars upward mid-year, creating yield volatility.

InvITs as a Capital Market Instrument

Perhaps the most significant capital markets dimension of asset monetisation is the rise of Infrastructure Investment Trusts (InvITs) as a distinct asset class in India. SEBI introduced the InvIT regulatory framework in 2014, but it was the government's active use of the structure — through PowerGrid InvIT in 2021 and NHAI InvIT subsequently — that gave the market genuine depth.

InvITs occupy a unique position in the investment universe: they offer quasi-bond-like predictable cash flows (from toll revenues, transmission charges, or pipeline tariffs) with a degree of capital appreciation upside. For institutional investors — particularly IRDAI-regulated insurance companies with long-duration liability profiles, and EPFO/NPS funds — InvITs are increasingly attractive as an alternative to G-Secs and corporate bonds.

The broader implication is significant: as the government monetises more infrastructure through InvITs, it effectively deepens the corporate debt and alternative assets market, providing a larger universe of investable instruments for domestic institutional investors. This is structurally positive for capital market development, even as it shifts yield-seeking demand away from traditional G-Secs.

Loan Portfolio Monetisation in the Banking Sector

A related but distinct form of monetisation operates within the banking system. When banks sell performing or sub-standard loan portfolios — as seen with Sammaan Capital's recent ₹5,000 crore sale to Arcil — they are monetising their balance sheet assets to free up capital for fresh lending. While this is governed by RBI's securitisation and asset reconstruction guidelines rather than the NMP framework, it reflects a similar logic of value extraction from existing assets. The RBI has progressively tightened the regulatory architecture around loan transfers to ensure that originators retain meaningful skin in the game, preventing the kind of originate-to-distribute excesses seen globally.

Risks, Criticisms, and the Road Ahead for India's Monetisation Strategy

Asset monetisation is not without its critics, and a balanced assessment demands engaging with the legitimate concerns raised by economists, trade unions, parliamentary committees, and civil society groups.

The Risk of Undervaluation

One of the most persistent criticisms is that public assets — built over decades with taxpayer money — may be transferred to private operators at below-fair-value concession fees, particularly when the bidding process lacks competition or when asset valuations are opaque. Unlike listed equity, where market prices provide a real-time benchmark, the valuation of a highway bundle or a gas pipeline is inherently complex and susceptible to information asymmetry between the government and potential bidders.

NITI Aayog and the Finance Ministry have emphasised the use of independent valuers, competitive bidding processes, and performance benchmarks embedded in concession agreements to mitigate this risk. However, the quality of implementation varies significantly across ministries and asset categories.

Monopoly Rents and Consumer Welfare

When a private operator takes over a public utility — a toll road, an airport, or a gas pipeline — the incentive to maximise returns can translate into higher user charges or reduced service quality for captive users who have no alternatives. This is particularly acute in sectors where infrastructure is a natural monopoly. Regulatory oversight by bodies such as the Airports Economic Regulatory Authority (AERA), the Petroleum and Natural Gas Regulatory Board (PNGRB), and state electricity regulatory commissions is essential to prevent rent extraction.

Critics also point out that monetising assets in perpetually profitable sectors (such as highways in dense urban corridors) essentially transfers a steady income stream from the public sector to private hands, raising questions about intergenerational equity.

Execution Risk and Contract Design

Even well-designed concession agreements can break down in practice. India's PPP history is replete with examples of projects that became financially stressed — due to traffic shortfalls, cost overruns, or regulatory changes — forcing renegotiation or government bailouts. If the private operator's projected revenues do not materialise, the government may face pressure to provide financial support or accept early exit of the concessionaire, undermining the entire monetisation rationale.

The Presumptive Taxation Dimension

An often-overlooked intersection of asset monetisation and tax policy relates to the treatment of income flows generated through these structures. The Income Tax Department's recent move to tighten disclosure norms under the presumptive taxation scheme for small businesses and professionals has broader implications for the SPV (Special Purpose Vehicle) structures and partnership arrangements that underpin many concession agreements. Greater scrutiny of related-party transactions and pass-through income within InvIT and REIT structures is a trend worth monitoring closely.

The Road Ahead: NMP 2.0 and Beyond

With the original NMP cycle (FY22–FY25) now concluded and progress mixed, the policy conversation has shifted toward a second-generation monetisation framework. Several imperatives will shape this evolution:

Expanding the asset universe: State-owned land banks, urban infrastructure held by municipal bodies, and assets of NABARD-funded rural infrastructure projects represent significant untapped potential that the original NMP did not comprehensively address.

Strengthening the regulatory ecosystem: SEBI's continued refinement of InvIT and REIT regulations — including minimum public float requirements, related-party transaction norms, and unit-holder rights — is critical to maintaining investor confidence.

State-level monetisation: Several state governments are now developing their own asset monetisation frameworks, particularly for roads, irrigation canals, and urban real estate. Coordination between central and state pipelines will be essential to avoid market saturation.

ESG and green infrastructure: As global and domestic institutional investors increasingly apply ESG (Environmental, Social, and Governance) screens, the monetisation of renewable energy assets — solar parks, wind corridors — is likely to attract premium valuations and deeper investor pools.

Conclusion: Asset Monetisation as a Structural Tool, Not a One-Time Fix

Asset monetisation in India has matured from a conceptual policy lever into an operational framework with measurable outcomes. At its best, it channels private capital and management efficiency into underutilised public infrastructure, generates non-debt receipts for the exchequer, and deepens India's capital markets through instruments like InvITs. At its worst, it risks transferring monopoly rents to private operators while leaving taxpayers with contingent liabilities and reduced public assets.

The success of the strategy ultimately depends on three variables: the quality of concession design, the robustness of regulatory oversight, and the government's ability to deploy monetisation proceeds into genuinely productive new investments rather than bridging current revenue gaps. For banking and finance professionals, the NMP and its successor frameworks represent not just a fiscal policy story, but a growing market opportunity — in InvIT underwriting, project finance advisory, stressed asset management, and institutional investment allocation.

As India's infrastructure ambitions continue to scale — with the Union Budget's capital expenditure targets rising each year — asset monetisation will remain an indispensable, if imperfect, tool in the government's fundraising arsenal. The challenge is not whether to monetise, but how to do it in a manner that is transparent, competitive, and genuinely value-accretive for the Indian public over the long term.